News

Profitable growth driven by strong technology uptake and improved performance across all segments

14 Nov 2024

FY2024 KEY ACHIEVEMENTS

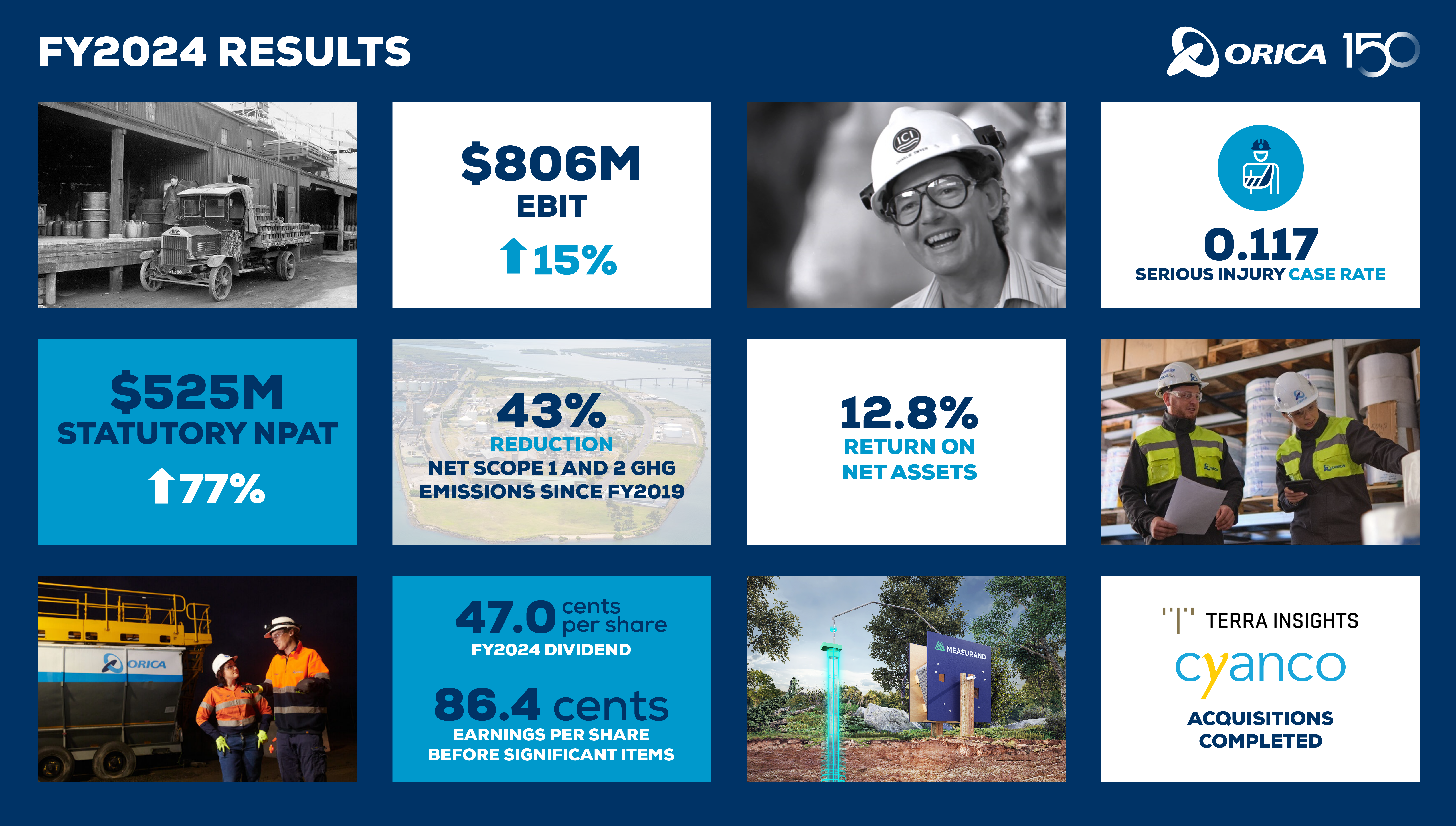

- Statutory Net Profit After Tax (NPAT)1 of $525 million (2023: $296 million), including $115 million of profit from significant items (SI)2 after tax

- EBIT3 of $806 million, up 15 per cent on the prior corresponding period (pcp)

- Earnings increased across all segments versus the pcp attributable to increased uptake of premium products and blasting technology, increased EBIT from Digital Solutions and contribution from two strategic acquisitions: Terra Insights and Cyanco

- Blasting Solutions EBIT of $755 million up 13 per cent on the pcp, driven by increased customer adoption of premium products, blasting technology and strong commercial discipline

- Specialty Mining Chemicals EBIT of $69 million up 36 per cent on the pcp, supported by the ongoing integration of the Cyanco acquisition

- Digital Solutions EBIT of $70 million up 29 per cent on the pcp, driven by continued strong adoption of digital solutions and supported by the ongoing integration of the Terra Insights acquisition

- Strong cash generation delivers net operating cash flow of $808 million (2023: $899 million)

- Earnings per share (pre-SI)4 of 86.4 cents, up 5.2 cents per share from the pcp

- Return on net operating assets (RONA)5 of 12.8%, up from 12.6% in FY2023

- Final dividend of 28.0 cents per ordinary share, unfranked, representing a payout ratio of 59%

- Successful delivery of the heavy turnaround schedule across Kooragang Island and Yarwun in Australia, and Carseland in Canada

- Execution of the first phase of the decarbonisation strategy ahead of schedule. Achieved a 43 per cent reduction in Scope 1 and 2 emissions from the restated baseline year (2019)

- Change of segment reporting completed following completion of the Cyanco acquisition in the Specialty Mining Chemicals segment, and the Terra Insights acquisition in the Digital Solutions segment

CEO Commentary

Summarising the continuing strong full-year performance, Orica Managing Director and CEO Sanjeev Gandhi said:

Safety and Sustainability

“Safety and the prevention of harm is the number one priority at Orica. Sadly, this year, we reported a fatality due to a collision on a public road in India6. We conducted a thorough investigation and implemented learnings across our operations.

“Our serious injury case-rate7 has improved over the last four years with a reduction from 0.210 in FY2021 to 0.117 in FY2024. Despite improvements, our key focus remains fatality prevention and the prevention of harm. There were no significant environmental incidents across our global operations in FY2024.

“This year represented one of our most significant years in terms of planned turnarounds at our manufacturing plants at Kooragang Island and Yarwun in Australia, and Carseland in Canada. The turnarounds were all completed safely, ensuring our manufacturing operations remain safe and efficient into the future.

“Ahead of schedule, we completed the first phase of our decarbonisation strategy in FY2024. The installation of two emissions abatement reactors at our Yarwun site is forecast to reduce the site’s total Scope 1 and Scope 2 emissions by 50 per cent from the 2019 baseline. The installation has accelerated delivery of our climate change commitments, resulting in our net operational Scope 1 and Scope 2 emissions being 43 per cent below our restated 2019 baseline.

“We are in a strong position to continue our momentum and drive further emissions reductions towards our climate targets across our entire value chain while creating more sustainable outcomes and offering our customers solutions that support their sustainability commitments.”

Strategy and Performance

“We have delivered another strong performance in the 2024 financial year with a 15 per cent growth in EBIT. Our team remains committed to executing our strategy and has delivered improved performance and growth across all segments again this year with a continued focus on quality of earnings.

“Increased uptake of premium products, blasting technology, digital solutions and contribution from the Cyanco acquisition has underpinned our performance this year.

“Our Blasting Solutions segment achieved strong earnings growth driven by commercial discipline and increased customer adoption of premium products and blasting technology including WebGen and 4D.

“Our newly established Specialty Mining Chemicals segment achieved earnings growth driven by the integration and delivery of the investment case for the Cyanco acquisition.

“Our Digital Solutions segment continues to deliver high growth, supported by strong customer demand, integration of Axis and Terra Insights and an improvement in segment performance measures, notably annual recurring revenue (ARR) and churn rate.

Terra Insights and Cyanco Update

“In 2024 we announced two strategic acquisitions: Terra Insights and Cyanco.

“The Terra Insights acquisition was completed on 29 February 2024 with ongoing integration into our business.

“We finalised completion of the Cyanco acquisition on 30 April 2024. Early integration success includes enhancing safety and reliability systems and processes, improving customer security of supply through global supply optimisation, and expanding Orica’s technology and services portfolio to further differentiate the Specialty Mining Chemicals customer offering. Integration activities will continue, and we forecast delivery of the investment case.

Dividend and Capital Management

The Board has declared an unfranked final ordinary dividend of 28.0 cents per share, representing a payout ratio of 59%. The dividend is payable to shareholders on 23 December 2024 and shareholders registered as at the close of business on 25 November 2024 will be eligible for the final dividend. This brings the full-year dividend to 47.0 cents per share, representing a full-year payout ratio of 56% per cent.

RONA increased from 12.6 per cent in FY2023 to 12.8 per cent in FY2024. Improved earnings performance driven by the execution of our strategy, and strong market demand supported this increased performance.

Gearing excluding lease liabilities8 at 26.2 per cent at 30 September 2024 is below our target range of 30 to 40 per cent.

FY2025 Outlook

- FY2025 EBIT is expected to increase on the prior corresponding period attributable to:

- Blasting Solutions: Demand expected to continue for premium products and blasting technologies, with full year benefits of the recontracting cycle.

- Specialty Mining Chemicals: Full year contribution from Cyanco, demand expected to grow in line with underlying market growth.

- Digital Solutions: Full year contribution from Terra Insights, continued strong adoption of technology solutions and cross-selling opportunities across the portfolio.

- Global support: Continued focus on cost initiatives to offset inflation and ongoing litigation costs.

- Ongoing challenges from inflationary pressures, higher energy costs and geopolitical risks.

- Capital expenditure (including acquisitions) expected to be broadly in line with FY24.

- Depreciation and amortisation expected to be $490 million to $510 million.

- Net finance costs expected to be $190 million to $200 million, primarily due to the full year impact of drawn debt to fund acquisitions.

- Effective tax rate to be broadly in line with FY24.

Looking forward

The outlook for the next three years is expected to deliver three-year average RONA in the range of 13.0 to 15.0(i) per cent (Previous range: 12.0 to 14.0(ii) per cent).

Commenting on the outlook for FY2025, Mr Gandhi said: “While we continue to make great progress executing our strategy and delivering continued quality earnings growth, we also remain deeply committed to continually improving our performance across all areas of our business.

“We expect the demand for our blasting solutions, specialty mining chemicals and digital solutions to continue to grow as we partner with our customers to satisfy their strong appetite for new technology and digital solutions.

“While inflationary pressures, higher energy costs and increasing geopolitical risks remain an ongoing challenge, our performance this year demonstrates our resilience and ability to adapt and mitigate ongoing macro-economic and geopolitical challenges.”

(i) FY2025–FY2027 three-year average RONA

(ii) FY2024–FY2026 three-year average RONA

1. Net profit after tax (NPAT) attributable to shareholders of Orica Limited, as disclosed in the financial statements in the FY2024 Annual Report.

2. Significant items (SI), as disclosed in note 1(e) in the financial statements in the FY2024 Annual Report.

3. Earnings before interest and tax (EBIT) or 'earnings' is equivalent to profit/loss before financing costs and income tax, excluding individually significant items, as disclosed in note 1(b) in the financial statements in the FY2024 Annual Report.

4. Basic earnings per share, (EPS), as disclosed in note 2 in the financial statements in the FY2024 Annual Report.

5. RONA is defined as earnings before interest and tax (EBIT) divided by rolling 12-month average net operating assets. Net operating assets include property, plant and equipment; intangible assets; investments in equity-accounted investees; trade working capital and non-trade working capital, excluding environmental provision - as disclosed in the financial statements in the FY2024 Annual Report.

6. Fatalities are reported as an Orica event following determination of work-relatedness (leveraging Occupational Safety and Health Administration guidelines) and where Orica has operational control of the area/activity. Non-work-related and third-party fatalities are recorded separately. Third-party fatalities are incidents that occur beyond Orica-controlled operations, environments and networks.

7. Serious injury case-rate (SICR) measures the total number of work-related Severity 3 and Severity 4 injuries per 200,000 hours worked by an employee and/or contractor.

8. Gearing is defined as net debt divided by the sum of net debt and total equity, where net debt excludes lease liabilities, as disclosed in note 3 in the financial statements in the FY2024 Annual Report.

Click here to view our FY2024 Annual Reporting Suite.

Andrew Valler

Andrew Valler

Media Contact

Head of Communications

Mobile +61 437 829 211

Natalie Worley

Investor Relations

Vice President

Mobile +61 409 210 462